Logistics Baba News, near the end of 2022, the freight volume in the container shipping market has rebounded again, and the freight rate has also shown signs of stopping the decline, but the market trend next year is still full of uncertainty. Freight rates are expected to plummet, “almost down to the variable cost range”. Since the release of epidemic control in China in December, there has been a wave of panic. At the end of December, the number of people working in factories and trading companies has dropped sharply by 1/3. It will take about 3-6 months for domestic and foreign demand to return to 2/3 of the level before the epidemic.

Since the second half of 2022, container shipping prices have been declining. Inflation, the Russo-Ukrainian war has suppressed the purchasing power of Europe and the United States, and the slow digestion of inventory has led to a significant decrease in freight volume. According to data released by the American research company Descartes Datamyne, the volume of containers sent from Asia to the United States in November was 1,324,600 TEU, a sharp drop of 21% year-on-year, which was greater than the 18% drop in October.

Since September this year, the decline in cargo volume has expanded. As of November, the volume of containers sent from Asia to the United States has declined year-on-year for the fourth consecutive month, highlighting the sluggish demand in the United States. In terms of loading destinations, China, with the highest ratio, saw a 30% reduction, the third consecutive month of reductions of more than 10%. Vietnam surged 26% due to a lower base period last year due to the expansion of the new crown epidemic last year, which led to stagnant production and reduced exports.

However, there has been a surge in the container shipping market recently, and Evergreen Shipping and Yangming Shipping’s U.S. lines have returned to full capacity. In addition to the effect of shipments before the Spring Festival, the continued unblocking of mainland China is also the key.

Container shipping companies believe that the global market is beginning to welcome a small peak season for shipments, but next year will still be full of challenges. Although there have been signs of a decline in freight rates, it is difficult to predict how much the rebound will be. The biggest key to the change in freight rates next year is that the IMO’s two new carbon emission regulations will come into effect, and the world will focus on the wave of ship demolition.

Large container shipping companies have begun to adopt various strategies to deal with the reduction in cargo volume. First, they have begun to adjust the operation mode of the Far East-Europe route. Some flights do not pay attention to speed. They choose not to pass through the Suez Canal, but instead go around the Cape of Good Hope and then to Europe. Such route adjustment will increase the sailing time from Asia to Europe by 10 days, which will not only save the Suez Canal toll, but also reduce the speed of sailing to meet the carbon emission regulations. Most importantly, the number of sailing days will increase, and the required ships will also be invested Climbing, indirectly diluting the newly invested capacity.

- Market demand will remain sluggish in 2023: Shipping prices will continue to fluctuate at low levels

“The cost of living crisis is eating into consumer spending power, resulting in reduced consumer demand for imported containerized cargo. There is no sign yet of a global solution to this problem, and we expect ocean freight volumes to decline.” Patrik “That said, if the economic situation worsens further, it could get worse,” Berglund predicted.

It is reported that for the development of the container shipping market next year, the shipping company ONE said that it is difficult to predict. After the spot freight rate and demand fell sharply, the container market has stagnated in the past few months. “Predicting the overall business environment has become more difficult in the face of increasing uncertainty,” the company said.

He outlined a series of risk factors: “For example, the ongoing Russia-Ukraine conflict, the impact of epidemic prevention policies, and labor negotiations at US-West ports.” In addition, there are three aspects that are particularly worrying.

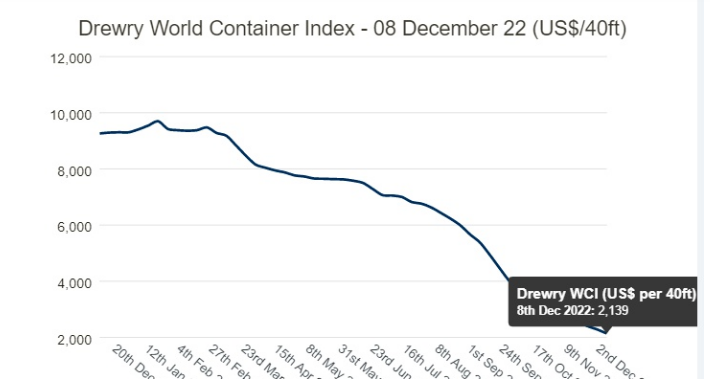

The spot freight rate plummeted: The SCFI spot freight rate reached its peak in early January this year, and after a sharp decline, compared with the beginning of January, the total drop reached 78%. Among them, the freight rate of the Shanghai-Northern Europe route has dropped by 86%, and the freight rate of the Shanghai-US West trans-Pacific route has dropped by 82%, and the price is US$1,423/FEU, which is 19% lower than the average freight rate from 2010 to 2019.

Things could get worse for ONE and other carriers. ONE expects operating costs to continue to rise and freight rates to continue to fall as inflation soars to double digits.

On the earnings side, will the expected decline from Q3 to Q4 continue at the same rate into 2023? “Inflationary pressures are expected,” ONE replied. The company has cut its earnings forecast for the second half of the fiscal year and said operating profit more than halved compared with the first half of this year and the second half of last year.

- Long-term contract prices are under pressure: shipping prices will continue to fluctuate at a low level

In addition, due to the sharp drop in spot freight rates, some shipping companies said that previous long-term contracts were required to be renegotiated to reduce prices. When asked if its customers were asking for a reduction in contract prices, ONE said: “When the current contract is about to expire, ONE will start discussing renewal with customers.”

Kepler Cheuvreux analyst Anders R.Karlsen said: “The outlook for next year is a bit bleak, contract prices will also start negotiations at a lower level, and the carrier’s earnings will normalize.” Alphaliner previously calculated, based on preliminary expected data reported by shipping companies , The revenue of shipping companies is expected to drop by 30%-70%.

The decline in consumer demand even means carriers are now “competing for volume,” according to Xeneta’s chief executive. Jørgen Lian, senior analyst at DNB Markets, predicts that the bottom line on freight rates in the container market will be tested in 2023.

James Hookham, chairman of the Global shippers’ Council, said in a quarterly review of the container shipping market released this week: “The big question going into 2023 is how much of their declining freight volumes will be committed to Contracts are being renegotiated, and how much volume will be reserved for the spot market. The spot market is expected to drop below pre-pandemic levels in the coming weeks.”

- More ships will go to sea in 2023: Shipping prices will continue to fluctuate at a low level

A flood of new containerships from shipyards will enter the market, while congestion and delays in container ports and supply chains are beginning to be resolved. Clarkson said new container ship orders from shipyards hit a record 7.4 million TEU in December. Many shipping lines have reaped handsome profits over the past two years and are converting some of their revenue into new tonnage, meaning increased capacity in the coming years.

“Overall, we think this will drive down freight rates to a level that exposes those carriers with the highest cost bases, and the risk of staggering revenues could quickly turn into a loss-making situation for carriers again,” Lian said.

ONE has commissioned 30 new ships, equivalent to 27.4% of its current fleet, and the company admits that more ships will be launched between next year and 2025.

“It is difficult to predict the future as old ships are demolished and new environmental regulations are implemented,” ONE said.